Renting After Bankruptcy or Foreclosure in Austin

How discharged bankruptcies and foreclosures are screened, which Austin properties weigh income over derogatory marks, and what documents help.

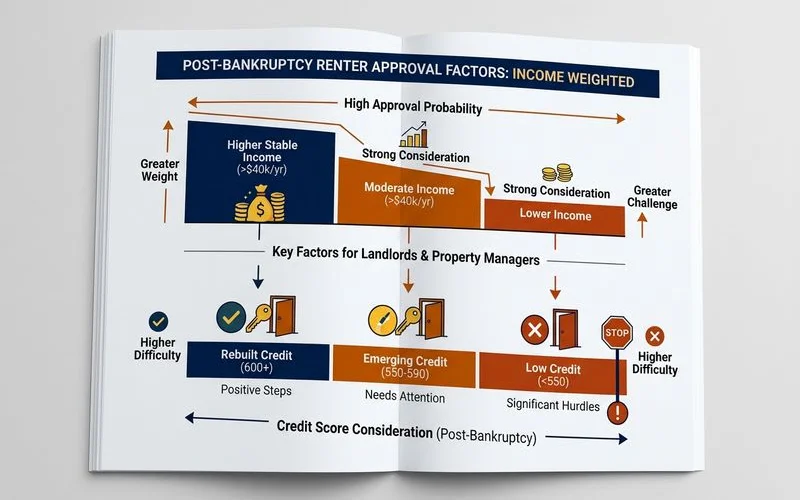

Bankruptcy and foreclosure are heavy credit events, but neither blocks apartment approval in Austin if you’re targeting the right properties. Many Austin communities — particularly income-focused complexes — recognize that a discharged bankruptcy is a closed chapter and weigh your current income more heavily than the underlying credit hit. Here’s how it works.

How bankruptcy shows up in screening

A bankruptcy filing appears on your credit report as a public record. The timeline:

- Chapter 7 bankruptcy stays on your credit report for 10 years from the filing date

- Chapter 13 bankruptcy stays for 7 years from the filing date

- Discharged status is noted on the report once the bankruptcy is complete

Apartment screening sees the bankruptcy entry but generally treats discharged differently from open or pending. Discharged means the underlying debts have been legally resolved; the slate has been cleared. Open or pending means the process is still in progress, which most properties treat more strictly.

Why discharged often reads better than open derogatory debt

This sounds counterintuitive but it’s how income-focused screening works:

- Open derogatory debt (collections, charge-offs, judgments) means there are creditors who haven’t been paid and might still come after you

- Discharged bankruptcy means those creditors have been legally barred from collecting; the debts are gone

A flexible community looking at two applications — one with $5,000 in open collections, one with a discharged Chapter 7 from 18 months ago — often prefers the discharged file. The risk is more bounded.

What to bring

For a post-bankruptcy application, prepare:

- Bankruptcy discharge papers (the official court document) — this is the single most important piece

- A list of discharged debts if you have one

- 4 weeks of recent pay stubs showing stable post-discharge income

- Employer letter with hire date — longer post-discharge employment reads better

- Bank statements for the last 2-3 months

- A short explanation letter with context (medical hardship, divorce, business failure)

If your bankruptcy was within the last 6 months, the pool is narrowest but still real. 6-24 months out: pool widens. 2+ years out: most income-focused communities work with you on the same standard application.

How foreclosure differs

Foreclosure is a separate event from bankruptcy (though they often follow each other). A foreclosure shows up as a specific credit event and stays on your report for 7 years.

Foreclosure doesn’t block apartment approval. It’s primarily a signal to mortgage lenders. Apartment screening treats it as a derogatory credit event but doesn’t usually weight it more heavily than a similar-aged bankruptcy.

If your foreclosure was a strategic decision (underwater home in 2009-era market), most flexible communities understand the context and treat it accordingly. If the foreclosure was tied to ongoing financial issues, the application may need more documentation.

Which Austin properties work with these cases

The pool of properties that work with post-bankruptcy or post-foreclosure files is roughly the same as the credit-flexible market generally:

- Older garden-style stock in South Austin and East Austin — most flexible

- Newer suburban mid-tier in Buda, Kyle, Pflugerville, Manor — income-focused screening, often very flexible

- Mid-rise complexes in central Austin that compete aggressively for tenants — case-by-case review more common

- Voucher-friendly properties — these communities are used to working with non-standard credit profiles

Strict Class A luxury and the most institutional portfolios are usually closed unless you’re 5+ years post-discharge.

What if you’re still in Chapter 13 repayment?

Chapter 13 is more nuanced. You’re typically in a 3-5 year repayment plan during which you make scheduled payments to creditors. Some properties will approve you while you’re in the plan, especially if you can show:

- Court approval to enter into a new lease (your trustee may need to sign off)

- Stable post-filing income at 3x rent

- A few months of plan payments made on time

A few Austin communities have explicit policies on Chapter 13 — they’ll approve if you can document the trustee’s awareness and your payment history. Your locator will know which.

How to make your case stronger

Two underused moves:

Letter of explanation: a one-page letter contextualizing the bankruptcy or foreclosure. Specific, factual, focused on what’s changed. “Medical bankruptcy due to a 2022 surgery. Stable employment since 2023. Discharged in 2024.” Doesn’t beg; explains.

Post-discharge tradelines: if you’ve opened a secured credit card or other small line of credit since discharge and have been paying on time, that’s evidence of stability. Pull a current credit report — even a 6-month history of on-time payments helps.

Ready to find Austin apartments that work with your post-bankruptcy or post-foreclosure file? Request your free list →

Frequently asked questions

Can I rent after a bankruptcy?

Yes. A discharged bankruptcy often reads more favorably than open derogatory debt because the legal cycle is complete and you have a documented fresh start.

Does a foreclosure block apartment approval?

Not at income-focused communities. Foreclosure is a credit event but it doesn't bar approval; properties weighing current income over past credit will work with you.

What documents help?

Bankruptcy discharge papers, proof of post-discharge income, an employment letter, and an explanation letter for context.

Ready for a curated bad credit list?

Tell us your situation. We'll send a list of Austin apartments that will approve you — in 24-48 hours, free, no upfront fees.

Get Your Free List