How to Dispute Wrongful Rental Debt in Texas

Contest inaccurate rental debt before you apply. FCRA dispute basics, Texas collection handling, how to request validation, and realistic timelines.

At Austin Second Chance Apartments, our team reviews hundreds of rental histories each year, and the sheer volume of inaccurate collection debt we see is staggering.

Many applicants assume these negative marks are permanent.

If you need to dispute rental debt collections texas agencies file against you, the right strategy makes all the difference.

We will break down the federal rules that make this possible, walk you through the exact steps to clear your record, and explain specific state laws that work in your favor.

The federal rule that makes this possible

The Fair Credit Reporting Act (FCRA) gives you the explicit right to dispute any inaccurate item on your credit report. This fcra rental debt dispute process is your strongest tool for removing invalid balances.

Our strategy relies on forcing collection agencies to prove their claims. The Consumer Financial Protection Bureau (CFPB) reported receiving nearly 4.8 million complaints about credit reporting issues in 2025 alone, showing exactly how common these reporting errors are. When you contest an account in writing, the following strict timeline applies:

- The collections agency has exactly 30 days to respond.

- They must produce complete validation of the debt.

- This validation must prove the requested amount is correct and they have the direct authority to collect it.

- If they fail to provide documentation, the entry must be removed from your report immediately.

- Even if they do validate the debt, you can still contest specific line items or the original lease enforceability.

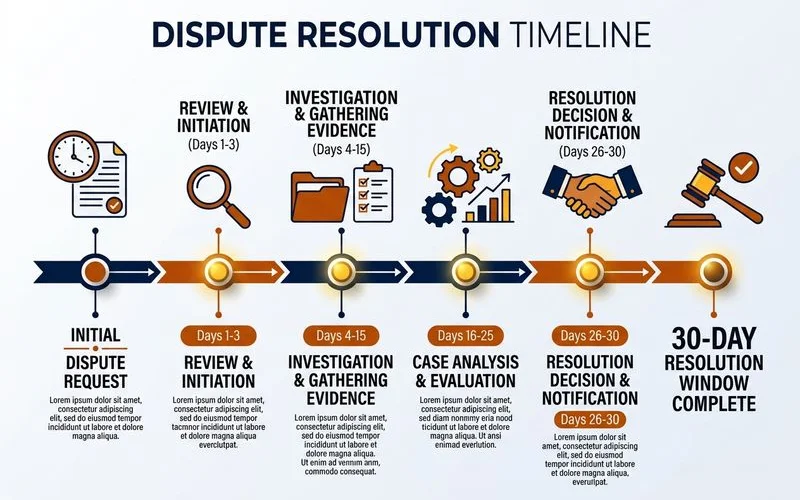

Step-by-step: how to dispute rental debt collections texas

Step 1: Pull all three credit reports

Get your free annual reports at annualcreditreport.com from Equifax, Experian, and TransUnion. These three bureaus frequently report the exact same debt differently.

We recommend checking each report for specific discrepancies in the balance, the date of last activity, and the listed agency. Over 80% of consumer complaints to the CFPB involve these top three agencies, making it highly likely you will find an actionable error. Note the exact details on each report to build a strong case.

Step 2: Write a debt validation letter

Send a written letter to the collections agency via certified mail with a return receipt. This legally required step creates a verifiable paper trail showing exactly when they received your demand.

Our clients often succeed by directly citing federal and state collection regulations. A proper texas debt validation letter must reference the specific account number and formally request proof under the Fair Debt Collection Practices Act (FDCPA).

Make sure your letter strictly demands the following items:

- Concrete evidence of the original debt amount.

- The complete chain of ownership from the apartment to the collection agency.

- Their specific legal authority and required state bond to collect in Texas.

Step 3: File a dispute with each credit bureau

File a dispute with each credit bureau reporting the debt while you wait for the agency to respond. You can initiate this parallel process online through the respective Equifax, Experian, or TransUnion portals.

We suggest stating clearly that the debt is inaccurate and unverified. The FCRA legally requires the bureau to investigate your claim within 30 days.

Step 4: Wait the 30 days

The law strictly enforces this 30-day investigation window. The entry stays on your report if the agency supplies the required documents within that timeframe.

Our experience shows that many agencies simply fail to respond in time. This failure to validate is incredibly common with specific types of accounts:

- Debts older than two or three years.

- Balances sold multiple times to different buyers.

- Accounts with missing original lease agreements.

Save copies of every single piece of correspondence for your records.

Step 5: Verify removal and re-pull your reports

Re-pull your credit reports after the 30-day window closes to confirm the deletion. Sometimes, a deleted collection account will unlawfully reappear later.

We help renters fight this illegal practice, officially known as re-aging. This constitutes a severe FCRA violation, and you can file an immediate complaint through the CFPB portal to force another permanent removal.

Texas-specific notes

Texas laws offer distinct protections that go far beyond standard federal statutes. Understanding these specific state codes is crucial for renters fighting unfair charges.

We always remind applicants about the Texas Property Code Section 92.104. This law requires landlords to provide an itemized list of any damage charges within 30 days of move-out. If they fail to send this list, you have strong legal grounds for a dispute.

Other critical state protections include:

- Texas Statute of Limitations: The Texas Debt Collection Act strictly sets the statute of limitations on most rental debt at four years from the date of last activity. Collectors cannot legally sue you in court after this time-barred period.

- Normal Wear and Tear: Texas law explicitly prohibits landlords from charging for normal wear and tear, such as faded paint or minor scuffs on a floor.

- Justice of the Peace Records: Eviction judgments stay accessible in JP court records indefinitely. These public court records are completely separate from your credit report.

- Itemization Rights: If a landlord does not provide the required damage list within the 30-day window, they legally forfeit the right to keep your deposit for those specific damages.

What to do while you wait

A pending dispute should not freeze your housing search. You can take proactive steps to secure an apartment while the 30-day clock runs.

We actively target properties with flexible screening policies for our clients. Your locator can identify management companies willing to approve applicants even with a disputed debt still showing on the report.

Save documentation of your dispute. A denied application can sometimes be overturned on appeal once the negative mark is officially removed.

Consider a guarantor program as a backup if the issue does not resolve within your required timeline.

When to get legal help

Consulting a consumer-protection attorney makes sense if the disputed amount is over $5,000 or if a collection agency sends threatening letters. Many specialized attorneys offer free initial consultations to review the facts of your case.

We highly recommend contacting organizations like Texas RioGrande Legal Aid and Lone Star Legal Aid for assistance. These non-profit groups provide free legal services for low-income renters facing aggressive debt buyers or active court judgments.

Tell us if you need to dispute rental debt collections texas agencies reported against you. We will target properties that work around an open dispute so you can keep moving forward. Request your free list →

Frequently asked questions

How do I dispute a rental collection?

Send a written dispute and a debt-validation request to the collections agency. Under the FCRA they must validate the debt within 30 days or remove it from your credit report.

How long does a dispute take?

Typically 30 days for the collections agency to respond. If they can't validate the debt, it must be removed. If they validate, you can still dispute specific charges.

Will disputing help me get approved?

Yes. Removing inaccurate debt or open collections clears a screening flag and can widen your property pool significantly.

Ready for a curated eviction list?

Tell us your situation. We'll send a list of Austin apartments that will approve you — in 24-48 hours, free, no upfront fees.

Get Your Free List