How Guarantor & Co-Sign Programs Get You Approved

LeaseLock, Rhino, and TheGuarantors can unlock approval after an eviction or rental debt. How co-sign programs work and what they cost.

We see perfectly capable renters get denied every single day because their application looks risky on paper. It happens when an eviction is recent or income sits just below the standard threshold.

This is exactly where a third-party guarantor steps in to flip that denial into an approval.

Finding a reliable apartment co-sign service austin renters can use is often the missing piece for a successful application. Let’s look at the data on lease guarantor programs austin property managers require, what they actually cost, and practical ways to use them to your advantage.

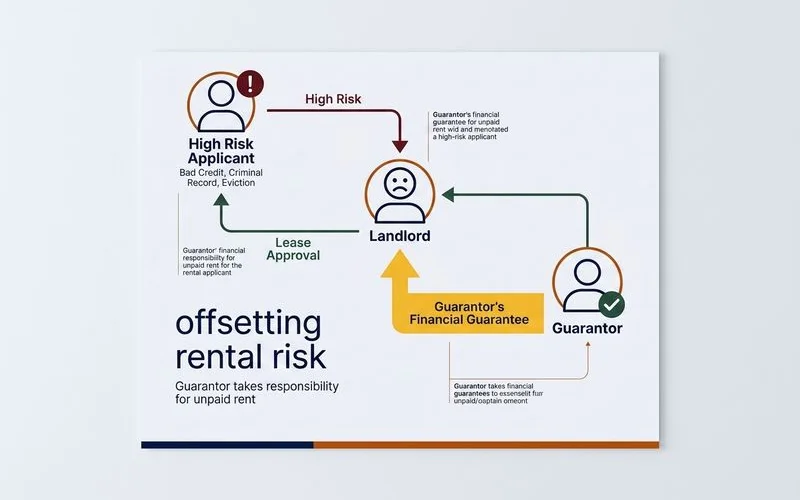

What a guarantor program actually does

A guarantor program is a financial product that insures the apartment community against rent loss and property damage. You pay a non-refundable fee, and the guarantor company issues a policy to the property manager. The company tells the community they will cover the bill if you fail to pay rent.

We track exactly how these providers operate across the Texas market. They take the financial risk out of the equation for the landlord. This converts a difficult application into a highly manageable one for you.

When comparing options like leaselock vs rhino, the differences come down to billing structures and coverage types.

| Provider | How It Works | Typical 2026 Pricing |

|---|---|---|

| LeaseLock | Embedded lease insurance automatically applied to borderline files. | $29 to $35 monthly fee. |

| Rhino | A la carte surety bond you set up directly with the community. | $10 to $30 monthly premium. |

| TheGuarantors | Premium rent and deposit coverage accepted by higher-end properties. | Roughly one month’s rent paid upfront. |

Our leasing team knows which properties accept which specific providers. Picking the wrong one wastes your application fee because landlords rarely accept a policy from a company they do not officially partner with.

What it costs

The cost ranges from a small monthly premium of $10 to $35, up to a single lump sum equal to one month’s rent. Pricing depends entirely on your specific applicant profile and the provider the building uses. A stronger applicant pays a lower premium, while a higher-risk applicant pays more.

Some communities split the upfront cost over the first three months of your lease. Other properties require the entire payment at the lease signing.

Monthly Premiums vs. Upfront Fees

Programs like Rhino and LeaseLock operate on a monthly model. You pay a smaller fee alongside your rent for the duration of your lease. Instead of a monthly charge, companies like TheGuarantors typically require a flat fee at the start.

We always remind clients that this fee is a non-refundable insurance premium. You do not get this money back at move-out the way you would with a standard security deposit.

Insider Warning: If your apartment uses a surety bond model like Rhino, the monthly fee does not erase your personal liability. If the landlord files a valid claim for damages when you move out, the insurer pays the landlord and then sends you a bill for that exact amount.

When a guarantor is required vs. optional

Communities force you to use a guarantor when your application flags their automated screening software. In Austin, standard income requirements sit firmly at three times the monthly rent.

We see automated systems like SafeRent immediately deny applicants who fall short of that multiplier. The software looks purely at the numbers before a leasing agent ever reviews your file.

Required: Property managers routinely mandate a guarantor when your file has one or more of the following issues:

- An eviction filing less than two years old (Travis County processed over 13,000 eviction filings recently, making this a common hurdle).

- Income sitting between 2x and 2.5x the rent amount.

- An outstanding rental debt over a specific community threshold.

- A bankruptcy or foreclosure within the past 12 to 24 months.

Strategic Uses for Approval

Sometimes adding a co-sign service is a smart move even if you technically qualify on your own. Our clients regularly use these programs to bypass massive deposit requirements.

Optional / strategic: Even when not strictly required, adding a guarantor makes sense to:

- Reduce a required cash deposit by 50% or more.

- Secure an approval for a premium unit where your credit score is borderline.

- Speed up the approval timeline during the competitive summer leasing rush.

How to set one up

You can secure a policy either directly through your leasing office or by applying independently on the provider’s website. The application process is typically 100% online and takes less than five minutes to complete.

We recommend checking with the property manager first to see which route they prefer.

There are two main paths:

- Through the community. Most flexible properties have an integrated system with a preferred vendor. The leasing office signs you up automatically during your application. That saves you from handling extra paperwork.

- Independently. You apply directly with a company like TheGuarantors to get pre-approved before touring. This strategy helps you understand your exact costs before committing to a specific unit.

If you have an eviction on your record, a broken lease, or significant rental debt, a guarantor is almost always part of the approval strategy. Our database tags every property on your curated list with their accepted providers so you never guess.

Common questions

Can I use a personal co-signer instead? Some properties do accept a personal co-signer, like a family member with strong credit and high income. Many institutional Austin communities only accept third-party guarantor programs because the financial payout is guaranteed.

We notice property managers prefer corporate guarantors because they eliminate the hassle of collecting debt from an individual. Corporate policies offer standardized protection.

Does a guarantor program show on my credit? No. These programs do not report as a loan or line of credit to the major credit bureaus. The fee goes directly to the insurance company rather than the apartment community.

Can I get out of a guarantor mid-lease? No. The premium covers the entire duration of your signed lease agreement. You cannot cancel the policy simply because your financial situation improves six months later. Some providers might refund unused portions if you transfer to a unit that does not require coverage, but that scenario is rare.

Ready to find out which Austin communities accept a lease guarantor programs austin for your situation? Request your free list →

Frequently asked questions

How much does a guarantor program cost?

Typically about one month's rent in fees, paid once. The fee insures the community against future rent loss, not against you.

Do all properties accept guarantor programs?

Many Austin properties do, but not all. Your locator targets communities that accept your specific guarantor provider (Rhino, LeaseLock, or TheGuarantors).

Does a guarantor guarantee approval?

It significantly improves the odds for riskier files, but each community still makes the final approval decision based on income and history.

Ready for your curated apartment list?

Tell us your situation. We'll send a list of Austin apartments that will approve you — in 24-48 hours, free, no upfront fees.

Get Your Free List