Does Paying Off a Broken Lease Help Approval?

When paying a broken lease balance helps vs. doesn't, the paid-vs-settled distinction, and how timing it before you apply changes your odds.

We hear this question from clients every single day.

If you have a broken lease balance owed to a former community, does paying broken lease help apartment approval? The answer is a definitive yes.

Our team at Austin Second Chance Apartments has helped thousands of renters rebuild their housing profiles. Getting past an automated denial requires understanding how property managers actually read your screening report. A recent review of 2026 data provides a clear roadmap for your next move.

We will break down the exact math behind paying, settling, or using a guarantor.

The short answer

Yes, paying off a broken lease balance directly improves your approval odds at the next apartment. A resolved account removes the automatic red flag that most leasing software programs use to reject applications.

Our agents see this play out constantly across Texas rental markets. Property management companies rely on automated platforms like RealPage and Experian RentBureau. These databases track your rental history for up to seven years.

We know an open debt triggers an immediate rejection. A zero balance changes the conversation entirely. The correct approach depends on four key variables.

- How much you owe changes the strategy entirely.

- Where the debt resides impacts your options.

- Your cash situation dictates what you can afford.

- Your timeline limits how fast bureaus update.

Paid in full vs. settled vs. open

We want you to understand exactly how these categories look to a leasing agent. Your broken lease balance will show up as paid, settled, or open on a background check. Each status carries a completely different weight during the tenant screening process.

Paid in full

We look closely at how property managers view settled vs paid rental debt. A paid status provides the strongest signal of financial responsibility. This is the cleanest status you can achieve.

Our agents verify that the community or collection agency updates the account to show a zero balance. You satisfy the debt completely. The automated screening algorithms instantly greenlight this result.

Settled

We consider a settlement to be the practical sweet spot for most renters. You negotiate a lower lump sum to close the account. Collection agencies operating in Texas routinely accept 40 to 70 percent of the original debt amount.

Our team has seen how much vastly superior this looks compared to an open collection account. The account officially closes with a “settled” or “paid as agreed” note. Paying a reduced portion still demonstrates a willingness to resolve past issues.

Open / in collections

We see automated screening software deny open accounts instantly. This represents the worst possible status for an applicant. The balance remains completely unresolved and actively damages your credit score.

Our advisors warn that the debt will stay on your record until you take action. An unresolved file leaves property managers with zero flexibility. Ignoring the balance guarantees a much harder apartment search.

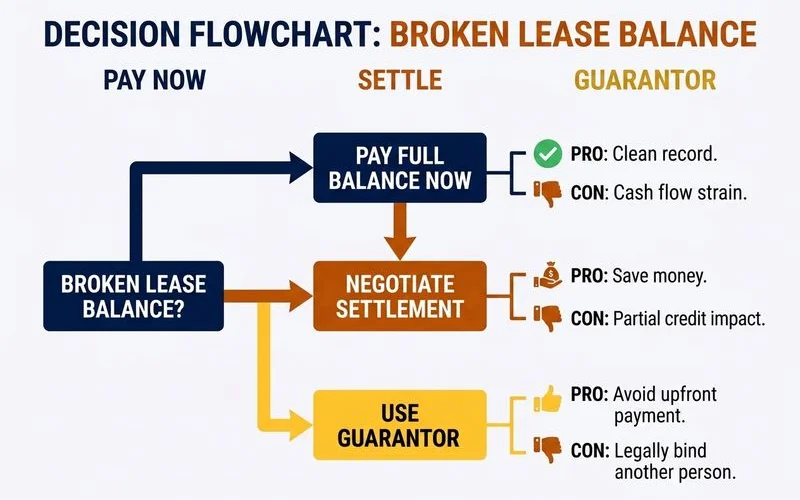

When paying makes the most sense

We recommend paying the full balance when the debt is relatively small. This approach completely clears your name without requiring complex negotiations. Paying directly ensures the fastest update to your screening profile.

Our clients typically choose this route under specific conditions.

- You owe less than $1,500.

- You can afford the payment without draining your deposit funds.

- The community you want uses strict AI screening tools like LeasingDesk.

- The debt remains with the original property manager.

- You have at least 30 days before submitting a new application.

When settling makes more sense

Settling for a lesser amount becomes the smarter move when your debt exceeds a few thousand dollars. This tactic saves your cash while still removing the active collection flag.

We suggest settling when you face large Texas Apartment Association reletting fees. These fees often hit 85 percent of a single month of rent. A negotiated settlement works best in these higher balance situations.

- Your total balance falls between $1,500 and $5,000.

- A third-party agency like National Credit Systems already owns the account.

- You must preserve cash for high Texas application and admin fees.

- You can negotiate the total down by at least 30 percent.

We tell every applicant to secure the agreement in writing before sending any money. The document needs to explicitly state the account will report as “paid as agreed” or “settled.” You must save that confirmation letter forever.

When a guarantor substitutes for paying

We frequently use a third-party guarantor for clients carrying massive rental debt. This alternative replaces the need to pay your old debt by insuring the new landlord against future losses. A bonding company steps in to cover up to three months of rent if you default.

Our target properties accept this coverage because it neutralizes their financial risk. This specific protection stops the exact risk that causes most application denials. A guarantor program makes sense when certain factors align.

- Your outstanding balance exceeds $5,000.

- You cannot realistically pay off a broken lease balance before moving.

- Your monthly income meets the new property requirement of 2.5x to 3x the rent.

- The target building accepts institutional providers like Rhino, LeaseLock, or TheGuarantors.

We want to clarify that a guarantee does not erase your old collection account. It simply bypasses the screening hurdle and opens the door to a new lease. The bonding provider usually charges a one-time fee equal to about one month of rent.

Our detailed guide explains the entire process. You can find a complete breakdown on how guarantor and co-sign programs work. Reading that resource will prepare you for the application step.

Timing the payoff

We advise renters to plan their moves around two distinct timeframes. Timing your payment correctly prevents you from getting denied for a debt you already resolved. Credit bureaus operate on a delay.

Credit bureau lag

Our tracking shows that paying a collection agency does not instantly update your credit profile. The major bureaus take 30 to 60 days to process the change. An eager applicant might submit paperwork on day 15 and still get denied.

We suggest allowing a generous buffer period before touring properties. Patience is mandatory during this update window. Applying too early wastes your hard-earned application fees.

Pay-for-delete agreements

We always encourage asking for a pay-for-delete agreement. Some collection agencies will erase the entry completely in exchange for payment. This strategy removes the negative tradeline from your report entirely.

Our agents have seen this tactic dramatically widen a client’s pool of available properties. You must demand this arrangement in writing before providing your debit card number. An erased entry reads even better than a “paid in full” status.

The math on paying

We always run the numbers before suggesting a specific path. Calculating your true costs requires looking at application fees, deposits, and settlement offers together. Settling an old debt improves your effective property pool by an estimated 30 to 50 percent.

Our math shows that if you only have $1,000 in cash and owe exactly $1,000, paying it all leaves you stranded. You need cash left over for your next move. Consider this specific strategy instead:

- Settle the old balance for $600 to save $400 immediately.

- Spend the remaining $400 on a third-party guarantor fee at a mid-tier property.

- Budget separately for the current average Texas application fees.

We want you to keep enough cash in reserve to cover standard non-refundable costs. The average application fee in Texas right now is $75 per adult. Property managers also charge a separate administrative fee ranging from $150 to $300. If your balance is tied to property damage rather than unpaid rent, our guide on renting with an unresolved lease or property damage covers how that changes the approval math.

Our specialists help you walk through this calculation on a free consultation call, and our broken lease apartment locator service matches you to communities that approve renters with an outstanding balance. The perfect combination always depends on your exact financial numbers. Ready for a curated list that matches your specific balance situation? Request your free list →

Frequently asked questions

Should I pay my broken lease balance before applying?

Usually yes if you can afford it — paid reads cleaner than open. Settled is the next-best, and a guarantor can substitute if cash is tight.

Is 'settled' as good as 'paid in full'?

Paid in full reads best. Settled (even for less than the full amount) reads as resolved and is meaningfully better than an open or in-collections balance.

How long before applying should I pay?

Pay or settle before you apply so screening reflects the resolved status. Allow 30-60 days for credit bureau updates if the debt was in collections.

Ready for a curated broken lease list?

Tell us your situation. We'll send a list of Austin apartments that will approve you — in 24-48 hours, free, no upfront fees.

Get Your Free List